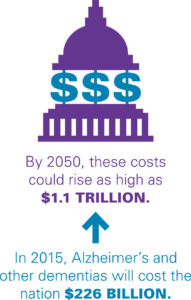

Taking care of a loved one with Alzheimer’s disease is daunting, emotionally and financially. The cost of Alzheimer’s care is skyrocketing, in fact, it is projected to surpass $277 billion, which is $20 billion more compared to last year.

To quote Keith Fargo, Ph.D., director of scientific programs and outreach for the Alzheimer’s Association:

“Soaring prevalence, rising mortality rates and lack of an effective treatment all lead to enormous costs to society, Alzheimer’s is a burden that’s only going to get worse. We must continue to attack Alzheimer’s through a multidimensional approach that advances research while also improving support for people with the disease and their caregivers.”

As the cost of Alzheimer’s rise, more families struggle to keep up resulting in keeping their loved ones at home. Although it is the cheapest option, in-home care might not be the best care setting for someone with cognitive impairment considering that this condition is progressive. So as the condition progress, a person with Alzheimer’s will gradually need more care and assistance in carrying out their activities of daily living (ADLs) – eating, bathing, toileting, dressing, transferring and incontinence.

Another downside of home care is it forces families to spend more time taking care of their loved one instead of working or worse they leave their jobs to become a full-time family caregiver. This is where a new problem arises that will eventually snowball into a massive financial problem for the caregiver. Due to the demand for caregiving, family members can’t properly plan for their potential care needs.

Since managing the hidden cost of Alzheimer’s care is overwhelming, we created this guide to help family members understand available long term care settings and services for people with Alzheimer’s, payment options and its financial impact.

How Much Does Alzheimer’s Care Cost?

Long Term Care

Based on the current cost of long term care in the United State, families who opt to keep their loved ones at home will pay about $4,114 per month for homemaker services and $4,222 per month for home health aide. The rest of the average monthly costs of long term care facilities are as follows:

- $8,365 per month in a private room in a nursing home.

- $7,362 per month in a semi-private room in a nursing home.

- $3,863 per month in a one-bedroom unit in an assisted living facility.

- $1,563 per month in an adult day health care.

View this interactive map to find the average cost of long term care in every U.S state.

Related: Infographic: Top 10 Cheapest Long Term Care in the United States 2018

Memory Care

If you find these rates expensive, all the more memory care, which provides comprehensive care to people with Alzheimer’s disease. It is more expensive compared to other care facilities. Its average cost is about $5,000 but it provides more effective and comprehensive care such as 24-hour supervised care for Alzheimer’s patients at all stages of Alzheimer’s.

Prescription Medications

A lot of people with Alzheimer’s would need prescription drugs such as Donezipil, Rivastigmate, and Galantamine also known as cholinesterase inhibitors. According to Consumer Reports, Alzheimer’s patients would need medications that would cost $150-$200 per month.

How To Pay for Alzheimer’s Care?

1. Out-of-the-pocket

Families usually pay for the cost of Alzheimer’s care out-of-the-pocket, which is too risky considering that the cost of care is rising. They end up dipping in their savings and withdrawing from their retirement accounts early.

In case individuals with Alzheimer’s are younger than 59 ½, they can withdraw from a retirement plan early such as IRA without incurring the 10% tax penalty.

Based on a survey of more than 3,500 Americans taking care of family members with Dementia, friends and family spent an average of more than $5,000 annually of their own money to pay for expenses such as food and diaper of their loved ones. You can read more startling facts here.

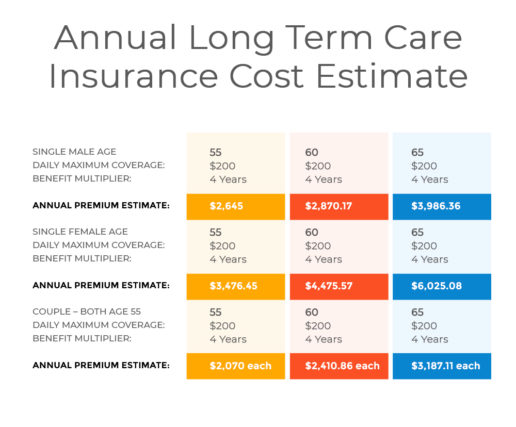

2. Long Term Care Insurance Policy

A long term care insurance policy is defined as a product that helps Americans fund their long term care needs due to an illness, accident or old age. It pays for long term care facilities such as nursing homes, assisted living facilities, CCRCs, adult day care, home care and etc.

If you want to protect your assets and spare your family from the emotional and financial implications of caregiving, you should consider buying a long term care insurance policy. The best time to buy coverage is when you’re in your 50s or when you’re young and healthy to make sure that your application for long term care policy will be accepted. Another advantage of buying early is to enjoy lower premiums.

Read Next: Top Reasons Why You Should Buy Long Term Care Insurance Before Age 50

3. Medicaid

Medicaid is a good option. Unfortunately, not all individuals with Alzheimer’s disease will be eligible for Medicaid benefits. Eligibility depends on the type, number, and extent of functional needs of Alzheimer’s patient. So, it’s best to contact your state to ask about the Medicaid eligibility requirements.

There are instances wherein a state extends its Medicaid benefits to individuals who require a certain level of care but they have assets that are above the state’s limit through pathways. Aside from asset requirements, pathways also require people to meet functional eligibility like the need for assistance with a definite number of ADLs.

4. Family Respite Care Grants

The Alzheimer’s Foundation of America (AFA) funds local, non-profit and member organizations through their Family Respite Care Grants. These grants are available through programs and organizations for families that are eligible for grants.

Through these programs, trained caregivers take care of an individual with Alzheimer’s to give family caregivers a time to take a break from caregiving or to attend to their personal needs. These grants are perfect for family members who are still working and saving for their future.

5. FLTCIP

A Federal Long Term Care Insurance Program (FLTCIP) is a long term care insurance policy for qualified members of the armed forces. However, not all who served the country are qualified for this program. Those who are in active duty and activated National Guard members ordered to work more than 30 days in a row, retired uniformed service members including retired and active duty members of the U.S. Army, U.S. Air Force, U.S. Navy, U.S. Marine Corps, U.S. Coast Guard, the Commissioned Corps of the U.S. Public Health Service and the Commissioned Corps of the National Oceanic and Atmospheric Association, and members of the Selected Reserve.

6. VA Benefits

Eligible veterans with Alzheimer’s or Dementia can receive in-home care, community-based, outpatient clinical care, nursing home, inpatient hospital care or hospice care through VA Benefits.

Conclusion

Paying for the high cost of Alzheimer’s disease is financially straining, the very reason why people should explore different payment options and programs as early as possible.

It’s important to understand all the options available and to start planning for care early to avoid financial woes and to avoid becoming an emotional and financial burden to your loved ones. So choose carefully among these payment options that can protect you and your loved ones from the devastating cost of Alzheimer’s care.